Oil Price

By Arthur Berman

Mar 22, 2017

I am tired of hearing about the unbelievable impact of

technology on collapsing U.S. shale production costs. The truth is that these

claims are unbelievable. The savings are real but only about 10 percent is from

advances in technology. About 90 percent is because the oil industry is in a

depression and oil field service companies have slashed prices to survive.

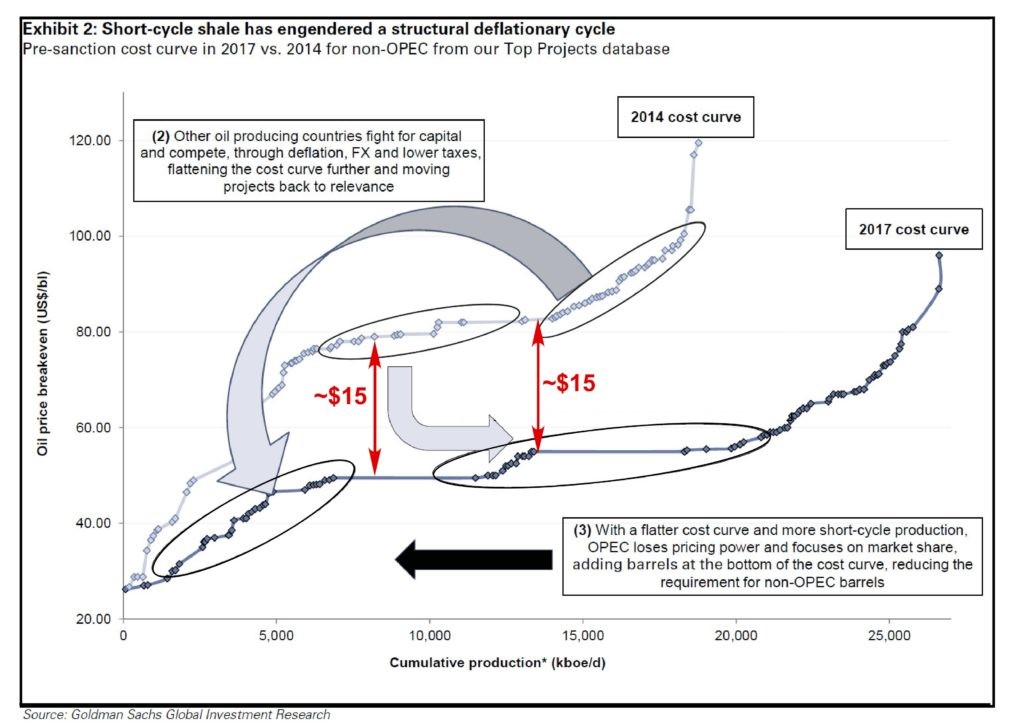

Zero Hedge posted an article yesterday called How OPEC

Lost The War Against Shale, In One Chart that featured the chart shown below

from a Goldman Sachs note.

Figure 1. Short-cycle shale has engendered a

structural deflationary cycle. Source: Zero Hedge and Labyrinth Consulting

Services, Inc.

Zero Hedge (and/or Goldman Sachs) erroneously states

that “the cost curve has massively flattened and extended as a result of shale

productivity.” If I read the chart correctly, the flat portion attributed to

“shale” represents ~ 10 mmb/d but tight oil only produces ~3 mmb/d.

This little arithmetic problem and the fact that the

entire 2017 cost curve has shifted downward ~$15/barrel from the 2014 curve

indicates that the true point and message of the graph is that break-even costs

for all producers have fallen almost 25 percent.

My business is working with clients who drill onshore

U.S. oil and gas wells. Rig rates have fallen 40 percent since the oil-price

collapse. One client had a bid for a drilling rig in September 2014 for $27,000

per day. By the time he signed the contract in March 2015, the rate was only

$17,000 per day. Another client recently ran a special high-tech log in a well

whose list price was $75,000 but he only paid $15,000 after discounts were

applied.

Most of the celebration of efficiency and productivity

is really about a depression in the oil industry that has resulted in massive

price deflation. I estimate that only about 10-12% of the cost reduction is

because of technology and most of that was a one-time benefit in the first year

or so it was used. Going forward, efficiency gains are a few percent at most.

“Our forecast assumes that

productivity declines 8% by the end of 2018…We believe a significant portion of

the productivity gains being experienced by the sector outside of the Permian

are the result of high grading and will revert in future years. Cost pressures

are already surfacing in the Permian, which will dampen capital efficiency

going forward.”

—Bernstein E&Ps ( 10 March 2017)

Break-even price is mostly a function of well cost,

flow rate and EUR.

I have already addressed well cost. Most companies and

analysts routinely exclude G&A (General and Administrative costs or

overhead), royalty payments, federal income taxes, depreciation and

amortization (“EBITDAX”) from their costs. Excluding cost is an excellent way

to reduce break-even price except that it does not accurately represent

break-even price….

To access the COMPLETE

news,

No hay comentarios:

Publicar un comentario